Ever wondered what makes up your property’s value? It’s more than just bricks and mortar!

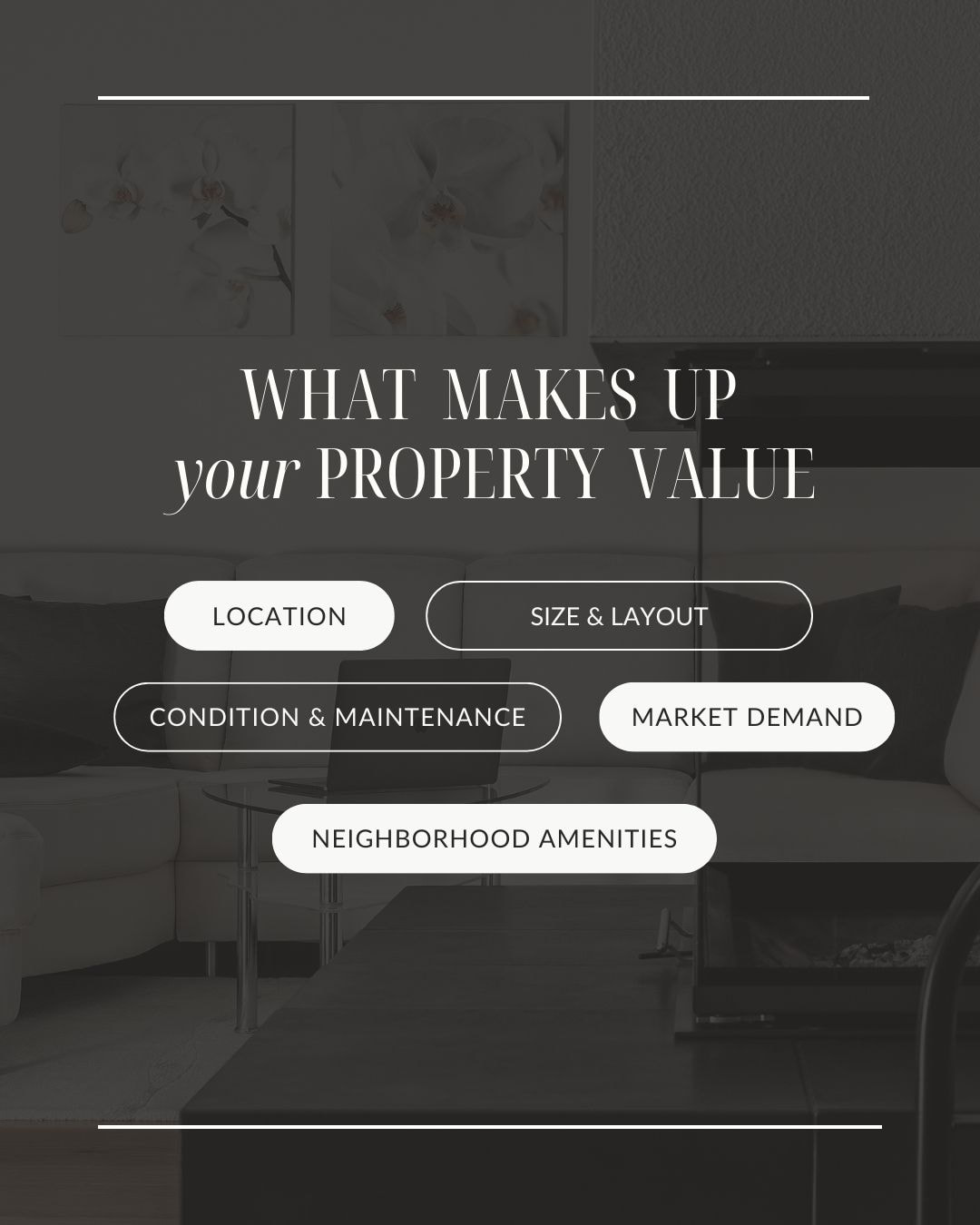

Property value is made up of: 1. Location, location, location 2. Size and layout 3. Market demand and trends 4. Condition and maintenance 5. Neighborhood amenities Understanding these factors can help you make informed decisions when buying or selling! When selling real estate, one of the most important decisions you'll make is the listing price. The right listing price can attract many potential buyers and lead to a profitable sale. On the other hand, if you set an unrealistic or too high of a listing price, it could keep away interested buyers and result in your property sitting on the market for months at a time with no offers in sight. Setting an accurate listing price is essential when it comes to maximizing your profits from real estate sales. There are several factors that affect the listing price of a property. One of the key factors is location, as it plays a significant role in determining the value of real estate. Properties in desirable neighborhoods or areas with high demand and limited supply will typically have higher listing prices than those in less sought-after locations. The size and layout of a property also contribute to its overall value, with larger homes and well-designed layouts generally commanding higher listing prices. The condition and maintenance of a property can also influence its listing price. A well-maintained property that requires minimal repairs or upgrades will typically have a higher listing price than one that needs extensive work. This is because buyers often take into account potential renovation costs when deciding on their offer for a property. Another crucial factor to consider when determining the listing price of a property is market demand. In a seller's market, where there are more buyers than available properties, sellers can generally set higher listing prices and still receive multiple offers. However, in a buyer's market, where there are more properties for sale than interested buyers, setting an appropriate listing price becomes even more critical as it can make or break a potential sale. Lastly, neighborhood amenities also play a role in determining the listing price of a property. Homes located near desirable amenities such as parks, schools, restaurants, and shopping centers will typically have higher listing prices due to their convenient location and added value. In conclusion, understanding what makes up your property's value is crucial when setting the right listing price. Factors such as location, size and layout, condition and maintenance, market demand, and neighborhood amenities all contribute to the final listing price of a property. As a seller, it's essential to carefully consider these factors before determining the listing price to ensure a successful sale in today's competitive real estate market. So do your research, consult with a trusted real estate agent or appraiser if needed, and set an accurate and attractive listing price that will generate interest from potential buyers and ultimately lead to a successful sale. So remember: setting the right listing price is key when it comes to selling your real estate property! Now that you have a better understanding of what goes into determining the listing price of a property, you can confidently make informed decisions when selling your real estate. I am always here to help you by providing a comparable market analysis and discuss with you your needs.

0 Comments

My First Home Purchase: What I Wish I Knew Beforehand

Buying a home is an exciting milestone and a long-term investment. For many people, the experience of buying their first home can be overwhelming. There are a lot of details to consider, from finding the right property to negotiating with sellers and taking out the mortgage loan. With so many aspects involved in buying a first home, it’s easy to get caught off guard by things you didn’t anticipate. Here are some of the surprises that came up for clients of mine during their process of buying their first home. The Cost of Moving When planning for their first home purchase, they were surprised by how much moving cost! From hiring movers to purchasing packing materials, the costs added up quickly. To reduce costs, they chose to do most of the packing themselves and borrowed furniture until they could afford new pieces for their new place. If you’re also planning on buying your first home soon, make sure you factor in these expenses when budgeting for your purchase. Added Expenses Associated with Home Ownership When they purchased their first house, one thing that surprised them was all the extra expenses associated with being a homeowner. In addition to paying your mortgage each month, there are also taxes associated with owning property as well as utilities bills and insurance premiums. Make sure you take all these bills into account when budgeting for your monthly expenses so that you don’t get overwhelmed down the line! The Lengthy Process Another thing that surprised them about buying their first home was how long it took! It seemed like every step in the process took longer than expected - from searching for properties online to actually signing off on paperwork at closing day! One way to speed up this process is to work closely with experienced real estate agents who can help guide you through each step without any hiccups along the way. Buying a house is an exciting milestone but it can also be overwhelming if you don’t know what to expect beforehand. As someone who just recently purchased their first house told me, there were definitely a few surprises along the way – from unexpected costs associated with both moving and homeownership to how lengthy this entire process was! If you’re about to embark on this journey yourself, make sure you set aside enough time and prepare yourself financially for what lies ahead so that everything goes smoothly! Give me a call and lets set up some time together to plan ahead.  How Much to Save for Closing Costs When Buying a Home

Closing costs are an unavoidable part of buying a home. Whether you’re a first-time homebuyer or you’ve been through the process before, it’s important to understand what closing costs are and how much money you should save to cover them. In this blog post, we will break down the basics of closing costs and help you plan accordingly. What Are Closing Costs? Closing costs is a term used to describe the various fees associated with purchasing a home. These fees include things like appraisal fees, escrow, title insurance premiums, interest, homeowners insurance, property taxes and more. While closing costs vary from state to state, they can typically range from 2.5% - 3% of the total purchase price of your home. For example, if you’re buying a $500,000 home in Oregon, you can expect your closing costs to be somewhere between $10,000 - $15,000. It’s important to note that these fees are usually paid at the end of the closing process when all documents have been signed and the deed has been transferred over to your name. How Much Should You Save? It’s always better to overestimate than underestimate when it comes to budgeting for closing costs. Depending on where you live and the type of loan you get (conventional or government-backed), your closing cost estimates could be higher or lower than expected. To make sure that you don’t come up short on moving day, it’s best practice to save enough money so that there are no surprises during the transaction process. As an example for Oregon buyers purchasing a $500K home: If you anticipate needing $12,500 in closing costs; it's recommended that plan for closer to $15K just in case unforeseen issues arise during inspection or escrow negotiations which could increase your total cost significantly above expectations. Closing costs can add up quickly and take many people by surprise when buying a new home—but that doesn't have to be the case! By doing your research ahead of time and planning accordingly for these additional expenses beyond just your down payment, you'll be able to focus on the excitement of becoming a homeowner without worrying about having enough cash on hand when it's time close escrow on your new property investment! Real estate buyers should save anywhere from 2.5%-3% of their total mortgage amount as an estimate for their eventual closing cost expenses depending on their location in order to ensure they have enough funds available at this critical stage in their purchase journey. With proper planning and budgeting these added expenses don't need to ruin anyone's dream of homeownership! |

Gabrielle Klink-ScudderBuilding relationships one home at a time. ArchivesCategories |

- HOME

- LISTINGS

-

Recently Sold

- 15631 S Rosemary Ct.

- 30920 S Dhooghe Rd

- 16811 SE 15th Street

- 695 River Drive

- 10117 NW Wilark Ave

- 15035 SE Pinegrove Loop

- 2220 E Gaither Avenue

- 721 SW Willowbrook Avenue

- 8811 NE 212th Avenue

- 1420 NE 20th Street

- 13565 SE Sherman Drive

- 809 Sitka Drive

- 708 NE 190th Avenue

- 13806 NW 10th Ct Unit C

- 1341 SE Jacquelin Drive, Hillsboro

- SELLERS

- BUYERS

- GET TO KNOW ME

- TESTIMONIALS

- BLOG

- HOME

- LISTINGS

-

Recently Sold

- 15631 S Rosemary Ct.

- 30920 S Dhooghe Rd

- 16811 SE 15th Street

- 695 River Drive

- 10117 NW Wilark Ave

- 15035 SE Pinegrove Loop

- 2220 E Gaither Avenue

- 721 SW Willowbrook Avenue

- 8811 NE 212th Avenue

- 1420 NE 20th Street

- 13565 SE Sherman Drive

- 809 Sitka Drive

- 708 NE 190th Avenue

- 13806 NW 10th Ct Unit C

- 1341 SE Jacquelin Drive, Hillsboro

- SELLERS

- BUYERS

- GET TO KNOW ME

- TESTIMONIALS

- BLOG

RSS Feed

RSS Feed